How to Set Up a Private Placement Data Room

A private placement data room is a secure virtual workspace where issuers share private placement memorandums, subscription agreements, and offering documents with qualified investors. This guide covers the document checklist by offering stage, Reg D and Reg S compliance structure, permission models for accredited and non-accredited investors, and how to run a data room that speeds up closings instead of slowing them down.

What Makes Private Placements Different from Other Data Rooms

Private placements are not fundraising rounds, and they are not M&A transactions. They sit in their own regulatory category, and the data room needs to reflect that.

In a typical VC fundraise, the data room supports a pitch. Founders share a deck, financial projections, and cap table with a handful of investors who have already expressed interest. The regulatory burden is low. In an M&A deal, the data room supports price discovery. Buyers dig through thousands of documents to validate an enterprise value. The regulatory burden is moderate.

Private placements are different because compliance is baked into the data room from day one. Under SEC Regulation D, issuers must verify investor accreditation status, file Form D within 15 days of the first sale, and maintain records that prove they followed the rules. A 506(c) offering where the data room lacks adequate accredited investor verification documentation exposes the issuer to rescission liability. That is a uniquely private-placement problem.

The scale is significant. Regulation D offerings raised $2.148 trillion in 2024, according to SEC Form D statistics. That is roughly 55 times the $39 billion raised through public IPOs in the same year. Despite being called "private," these transactions represent the dominant capital-raising mechanism in the United States. The documents behind those offerings need infrastructure that matches the stakes.

Private placement data rooms also serve multiple investor classes simultaneously. A 506(b) offering might include both accredited and non-accredited sophisticated investors, each requiring different disclosure levels. A dual Reg D and Reg S offering needs separate document sets for domestic and offshore investors. The permission model has to handle this complexity without creating operational chaos.

Document Checklist by Offering Stage

The biggest organizational mistake issuers make is dumping every document into a single folder and granting blanket access. Private placements have distinct phases, and each phase requires a specific document set.

Pre-Offering Preparation

Before any investor sees the data room, these documents should be finalized and uploaded:

- Private Placement Memorandum (PPM) with all risk factors, use of proceeds, and offering terms

- Subscription Agreement and Investor Questionnaire

- Certificate of Incorporation or Formation documents

- Operating Agreement or Limited Partnership Agreement

- Board resolutions authorizing the offering

- NDA or Confidentiality Agreement template

- Cap table showing current ownership structure

Active Offering Phase

Once the offering is live and investors are reviewing materials, add:

- Audited financial statements for the prior two to three years

- Unaudited management accounts (current quarter)

- Financial projections and fund model with waterfall calculations

- Material contracts (customer, vendor, licensing agreements)

- Related-party transaction disclosures (three years)

- Team biographies and background check certifications

- Pitch deck or investment thesis presentation

- Form D filing (draft or final, depending on timing)

Compliance and Verification

This folder is the legal backbone of your offering. Every document here is a potential exhibit in an SEC inquiry:

- Accredited investor verification records (third-party letters, minimum investment confirmations, or financial document reviews)

- AML and KYC documentation for each investor

- State Blue Sky notice filings for each jurisdiction where investors reside

- Placement agent agreements (if a broker-dealer is involved)

- FINRA broker-dealer confirmations

Post-Close and Investor Relations

The data room does not shut down after the offering closes. Private placements often require ongoing investor communication:

- Capital call notices and distribution statements

- Quarterly or annual LP reports

- Updated financial statements

- Amendments to the PPM or Operating Agreement

- K-1 tax documents

A clear folder numbering system keeps this manageable. Use numbered top-level folders (01-Offering-Documents, 02-Legal-Corporate, 03-Financials, 04-Compliance, 05-Team, 06-Presentations, 07-Investor-Correspondence) so investors can orient themselves without asking where to find the subscription agreement.

Reg D Compliance Structure

The choice between Rule 506(b) and Rule 506(c) determines how your data room is organized, who can access it, and what verification records you need to maintain.

Rule 506(b) Offerings

Under 506(b), issuers can raise unlimited capital from an unlimited number of accredited investors plus up to 35 non-accredited but sophisticated investors. No general solicitation or advertising is allowed. Self-certification is sufficient for accredited investor status: investors check a box on the subscription agreement confirming they qualify, and the issuer does not need to independently verify unless there is reason to doubt the representation.

The data room implication is that non-accredited investors must receive full disclosure documents, including financial statements meeting specific SEC requirements. Your permission model needs at least two tiers: one for accredited investors with standard access, and one for non-accredited investors with expanded disclosure materials.

Rule 506(c) Offerings

Under 506(c), all purchasers must be accredited investors with no exceptions, but general solicitation and advertising are permitted. The trade-off is that independent verification of accredited status is required. Historically, this meant reviewing tax returns, W-2s, bank statements, or obtaining verification letters from CPAs, attorneys, or broker-dealers.

In March 2025, the SEC issued guidance that simplified verification for 506(c) offerings. Issuers can now rely on a minimum investment amount as a reasonable verification step: $200,000 for natural persons and $1,000,000 for legal entities, provided the investor represents in writing that they are accredited and that their investment is not financed by a third party. For many institutional offerings with high minimums, this eliminates the need to collect personal financial documents.

Your 506(c) data room should include a dedicated verification subfolder for every investor, containing the signed representation, third-party verification letter, or minimum investment confirmation. This folder is your defense in any SEC inquiry.

Regulation S for Offshore Investors

If you are running a concurrent Reg S tranche for non-US investors, the data room needs a separate access tier. Reg S documents include offshore investor certifications, representations that investors are non-US persons, and transfer restriction legends on securities. No marketing activity can be directed toward the US market for the Reg S portion. Keep the document sets isolated so there is no accidental cross-contamination between domestic and offshore materials.

Set Up Your Private Placement Data Room Today

Fastio gives you granular permissions, audit trails, and AI-powered document search with generous storage. No credit card, no trial period.

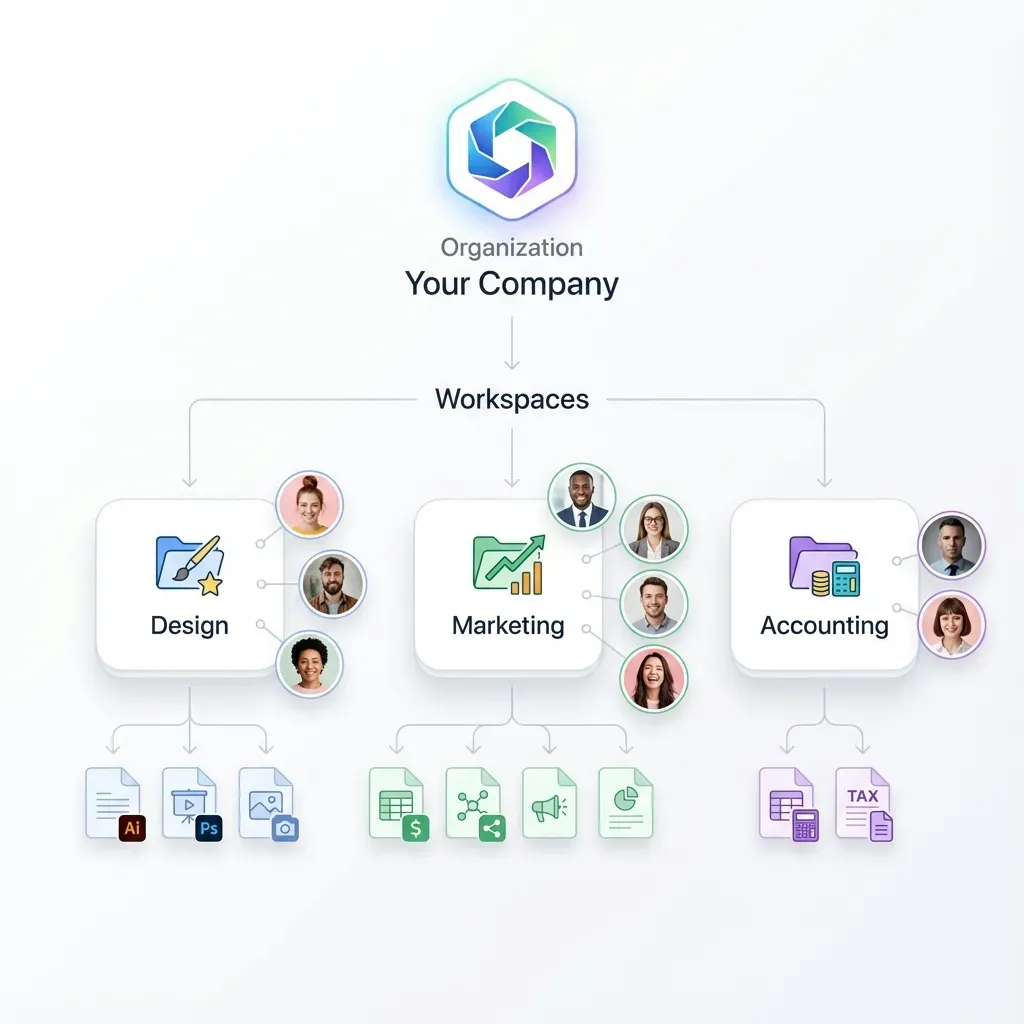

Permission Models and Access Controls

Private placement data rooms serve multiple parties with different information needs and legal entitlements. The permission structure needs to reflect these differences without creating administrative overhead that slows down the offering.

Tiered Access by Investor Class

At minimum, you need these permission groups:

Accredited investors (domestic) get access to the PPM, subscription agreement, financial statements, team materials, and presentation deck. They do not need the expanded disclosure documents required for non-accredited investors under 506(b).

Non-accredited sophisticated investors (506(b) only) get everything accredited investors see, plus the additional financial disclosures mandated by Regulation D. These typically include audited balance sheets and income statements meeting the specific format requirements in Rule 502(b).

Offshore investors (Reg S tranche) get a separate document set with offshore-specific representations and certifications. Their access should not include any US-directed marketing materials.

Legal counsel and advisors may need broader access for due diligence review, but should be restricted from downloading or printing certain documents unless specifically authorized.

Placement agents need access to marketing materials and investor tracking data, but may not need the detailed financial models or internal projections.

Practical Controls That Matter

Beyond user-level permissions, several controls are essential for private placement compliance:

NDA gating means no investor gets data room access before a signed confidentiality agreement is on file. This is especially important for 506(b) offerings where general solicitation is prohibited. If an unsigned party accesses your materials, it could be construed as a public offering.

Document-level watermarking with the investor's name and email on downloaded PPMs and financial statements deters unauthorized sharing. Dynamic watermarks that render at download time are more effective than static overlays.

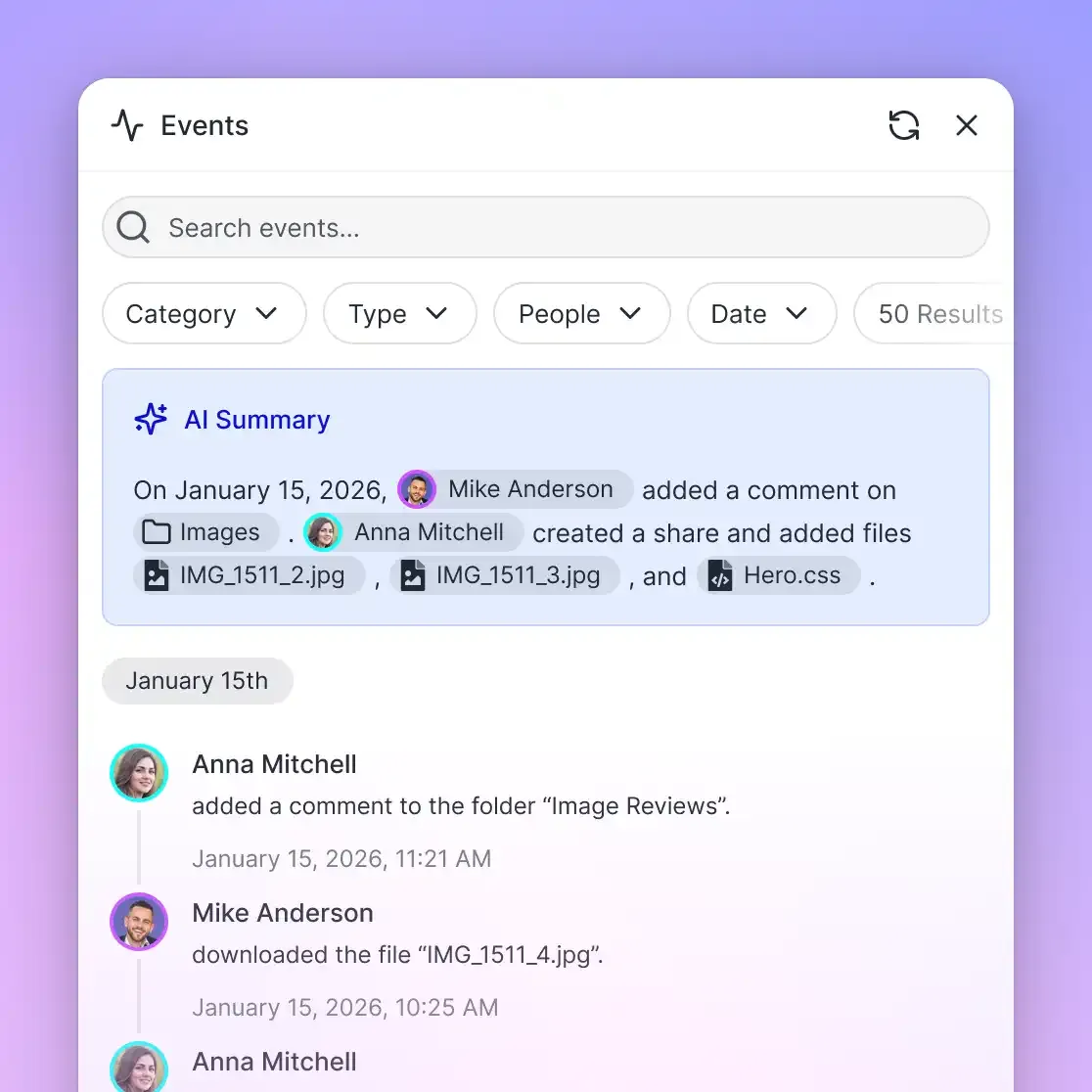

Audit trails that log every login, document view, download, and print are not optional. Under Reg D, if you provide material information to one investor, that information should be made available to all investors in the same class. Your audit log is the record that proves consistent disclosure.

Link expiration tied to offering timelines prevents stale access. When the offering closes or an investor withdraws, revoke access immediately. Set default expirations that match your NDA terms.

Fastio handles these requirements through its workspace and share system. Granular permissions operate at the org, workspace, folder, and file level, so you can build the tiered access model without creating separate data rooms for each investor class. Audit trails capture every action, and share links support passwords, expiration dates, and domain whitelisting. Intelligence Mode adds semantic search on top, so investors and counsel can ask questions about the documents and get answers with citations to specific pages, without needing to open every PDF individually.

Running the Offering Process

A private placement data room is not a static document repository. It is an operational tool that changes throughout the offering lifecycle. How you manage it during the live offering affects closing speed and compliance posture.

Pre-Launch Preparation Before granting any investor access, complete these steps:

Upload all pre-offering documents and verify that the folder structure matches your document index. Create a root-level index document that explains the structure, lists key contacts for questions, and provides a timeline for the offering. Test permissions by accessing the room from an external account to confirm that each investor tier sees the correct document set and nothing more.

Name files consistently. "2026-Q1-Audited-Financials.pdf" is immediately scannable. "final_v3_REVISED_TOM.pdf" is not. Convert documents to PDF format for consistent rendering across devices, and run OCR on any scanned pages so they are searchable.

During the Active Offering

Maintain a formal Q&A log. When an investor asks a question about the PPM or financials, the answer goes into the log and becomes available to all investors in the same class. This is not just good practice. Under Reg D, material information provided to one investor should be disclosed to all investors.

When the PPM is amended (common in offerings that run for several months), have a protocol for notifying all investors and updating the data room. Document who was notified, when, and how. The amendment notice should be uploaded alongside the revised PPM, not substituted silently.

Track engagement data. Which investors are spending time in the financials folder? Which opened the PPM once and never returned? This data shapes your follow-up strategy and helps your placement agent focus on investors who are actively conducting diligence rather than those who are window-shopping.

Closing and Post-Close

When the offering closes, archive the data room in its final state before making any changes. This snapshot is your evidentiary record if a dispute arises about what was disclosed, when, and to whom. Then transition the room to its post-close function: ongoing investor relations, capital call documentation, and periodic reporting.

Do not delete the room. The statute of limitations on securities fraud claims is five years from the violation, and many disputes surface well after closing. Your archived data room, with its complete audit trail, is your best evidence that the offering was conducted properly.

Choosing a Data Room Provider

Not every virtual data room is built for private placements. Many VDR providers optimize for M&A deals, where the primary need is bulk document storage with basic access controls. Private placements have additional requirements that narrow the field.

What to Evaluate

Tiered permissions at the folder and file level. Room-level permissions are insufficient for private placements. You need to control access by investor class, and that means granular controls on individual folders and documents within the same room. If a provider only offers "admin" and "viewer" roles, it will not work for a multi-class offering.

Compliance-grade audit trails. Every login, view, download, print, and permission change must be logged with timestamps and exportable in CSV or JSON format. This is your compliance documentation for SEC inquiries. Basic "last accessed" timestamps are not enough.

Watermarking and download controls. Dynamic watermarking with the viewer's identity on sensitive documents is important for PPMs and financial statements. The ability to disable downloads entirely for certain document classes while allowing viewing gives you fine-grained control over document distribution.

Search across all documents. Investors and their counsel will need to find specific clauses, figures, or risk factors across hundreds of pages. Full-text search, including OCR for scanned documents, is the feature that separates a data room from a shared folder.

API and webhook support. If your offering involves a placement agent or CRM system, the data room should works alongside those tools. Webhooks that fire when an investor downloads the subscription agreement or views the financial model let your team respond in real time.

Provider Options

Traditional VDR providers like Intralinks,

Datasite (formerly Merrill), and Firmex focus on M&A and tend to charge per-page or per-user pricing that can run into thousands of dollars per month for large offerings. They offer strong compliance features but at enterprise price points.

Mid-market options like iDeals and DealRoom provide similar functionality at lower price points, often with flat-rate monthly pricing. They work well for offerings with moderate document volumes.

Fastio takes a different approach with usage-based pricing and a free tier that includes 50 GB of storage with no credit card required. Workspaces support granular permissions at the org, workspace, folder, and file level. Shares can be configured as Send, Receive, or Exchange workflows with passwords, expiration dates, and domain whitelisting. Intelligence Mode auto-indexes uploaded documents for semantic search, so investors can ask natural language questions about the PPM and get answers with citations to specific pages. The platform is not a traditional VDR, but for issuers who need secure document sharing with strong access controls and built-in document intelligence, it covers the core requirements at a fraction of the cost.

Helpful references: Fastio Workspaces, Fastio Data Rooms, and Fastio AI.

Frequently Asked Questions

What documents go in a private placement data room?

The core documents include the Private Placement Memorandum (PPM), subscription agreement, investor questionnaire, cap table, audited financial statements, formation documents, operating or LP agreement, board resolutions, team biographies, and a pitch deck. You also need a compliance section with accredited investor verification records, AML/KYC documentation, Blue Sky state filings, and Form D filing records.

How do you share a PPM with investors securely?

Upload the PPM to a virtual data room with folder-level permissions, require a signed NDA before granting access, enable dynamic watermarking with the investor's name on downloads, set link expiration dates tied to your offering timeline, and maintain audit trails that log every view and download. For 506(b) offerings, restrict access to avoid anything that could be construed as general solicitation.

What is the difference between a private placement and fundraising data room?

A fundraising data room supports a pitch to investors, typically with a deck, financial projections, and cap table. A private placement data room must also satisfy SEC regulatory requirements from day one, including accredited investor verification, Form D filing records, Blue Sky state notices, and tiered access controls for different investor classes. The compliance documentation is the primary difference.

Do I need a data room for a Reg D offering?

Technically, no. There is no legal requirement to use a virtual data room for Reg D offerings. However, the compliance documentation requirements (audit trails, investor verification records, consistent disclosure to all investors) make a VDR the practical standard. Sharing a PPM over email with no tracking creates compliance risk if the SEC later asks you to prove what was disclosed, to whom, and when.

How long should I keep the private placement data room after closing?

At minimum, five years after the offering closes. The statute of limitations on securities fraud claims under federal law is five years from the violation. Many practitioners keep data rooms archived indefinitely, since storage costs are minimal and the evidentiary value of a complete audit trail far outweighs the cost of maintaining it.

What changed with SEC 506(c) verification in 2025?

In March 2025, the SEC issued guidance allowing issuers to use a minimum investment amount as a reasonable verification step for accredited investor status. Natural persons investing $200,000 or more, or entities investing $1,000,000 or more, can self-certify their accredited status in writing, provided they also represent that their investment is not financed by a third party. This reduced the administrative burden for offerings with institutional-level minimums.

Related Resources

Set Up Your Private Placement Data Room Today

Fastio gives you granular permissions, audit trails, and AI-powered document search with generous storage. No credit card, no trial period.