How to Set Up a Data Room for Private Credit Transactions

A data room for private credit is a secure virtual workspace where direct lenders and borrowers share loan documentation, financial statements, and covenant compliance records during credit transactions. This guide covers the document checklist specific to private lending, folder structure for multi-tranche deals, permission models for syndicated credit facilities, and how to track lender engagement throughout due diligence.

Why Private Credit Needs a Different Data Room

Most data room guides assume you're running an equity transaction. A founder raising venture capital needs a pitch deck, cap table, and growth metrics. A company going through an M&A process needs financial statements, customer contracts, and IP documentation. Private credit transactions share some of those documents, but the core of the diligence process looks fundamentally different.

Private credit lenders care about repayment capacity, not growth potential. They want to see cash flow projections under stress scenarios, detailed collateral schedules, and the legal framework governing their priority position relative to other creditors. The global private credit market reached $3.5 trillion in assets under management by late 2024, a 17% increase from the prior year, and capital deployment hit $592.8 billion in 2024 alone. That volume of lending activity means lenders are reviewing dozens of deals simultaneously. A disorganized data room doesn't just slow things down. It signals that the borrower may not be organized enough to manage ongoing reporting obligations.

The document set for a private credit deal typically runs between 200 and 800 files, depending on the complexity of the facility and the number of borrower entities involved. Direct lending transactions involve a single lender or small club, while broadly syndicated deals can involve ten or more participating institutions. Each participant needs access to different document sets at different stages, and the data room needs to handle that access control cleanly.

The distinction matters for how you organize the room. Equity data rooms emphasize narrative and market opportunity. Private credit data rooms emphasize verifiability: your financial covenants, your collateral coverage ratios, and your track record of timely reporting.

Helpful references: Fastio Workspaces, Fastio Collaboration, and Fastio AI.

Document Checklist for Private Credit Data Rooms

Private credit due diligence follows a structured process, but the specific documents differ from equity transactions. Here's what lenders expect to see, organized by category.

Credit Agreement Documentation -

Draft or executed credit agreement (term sheet, commitment letter)

- Intercreditor agreement (for facilities with multiple lien positions)

- Security agreement and collateral descriptions

- Guaranty agreements from parent entities or subsidiaries

- Subordination agreements (if junior debt exists)

- Fee letters and closing checklists

Borrower Financial Information - Audited financial statements (three years minimum)

- Monthly or quarterly management accounts (trailing twelve months)

- Financial model with base case, upside, and downside scenarios

- Cash flow projections tied to debt service coverage

- Working capital analysis

- Capital expenditure history and forward budget

- Tax returns (three years)

Collateral and Security Package

Loan tape (detailed schedule of receivables, loans, or assets pledged)

- Borrowing base certificate (current and historical)

- Collateral appraisals and valuations

- UCC filing confirmations

- Title reports and lien searches

- Insurance certificates covering pledged assets

Covenant Compliance

- Covenant compliance certificates (historical)

- Debt service coverage ratio calculations

- use ratio calculations

- Fixed charge coverage computations

- Covenant waiver or amendment history

Legal and Corporate

Corporate organizational documents (charter, bylaws, operating agreements)

- Organizational chart showing all entities in the borrower group

- Material contracts and customer agreements

- Pending or threatened litigation

- Regulatory licenses and permits

- Environmental assessments (if applicable to collateral)

Existing Debt

- Schedule of all existing indebtedness

- Current debt agreements and amendments

- Payoff letters for debt being refinanced

- Subordination or intercreditor agreements with existing lenders

This checklist covers the core documents for a direct lending transaction. Syndicated deals add information memorandums, bank meeting presentations, and lender voting agreements. Asset-backed facilities add detailed loan tape specifications and servicer performance data.

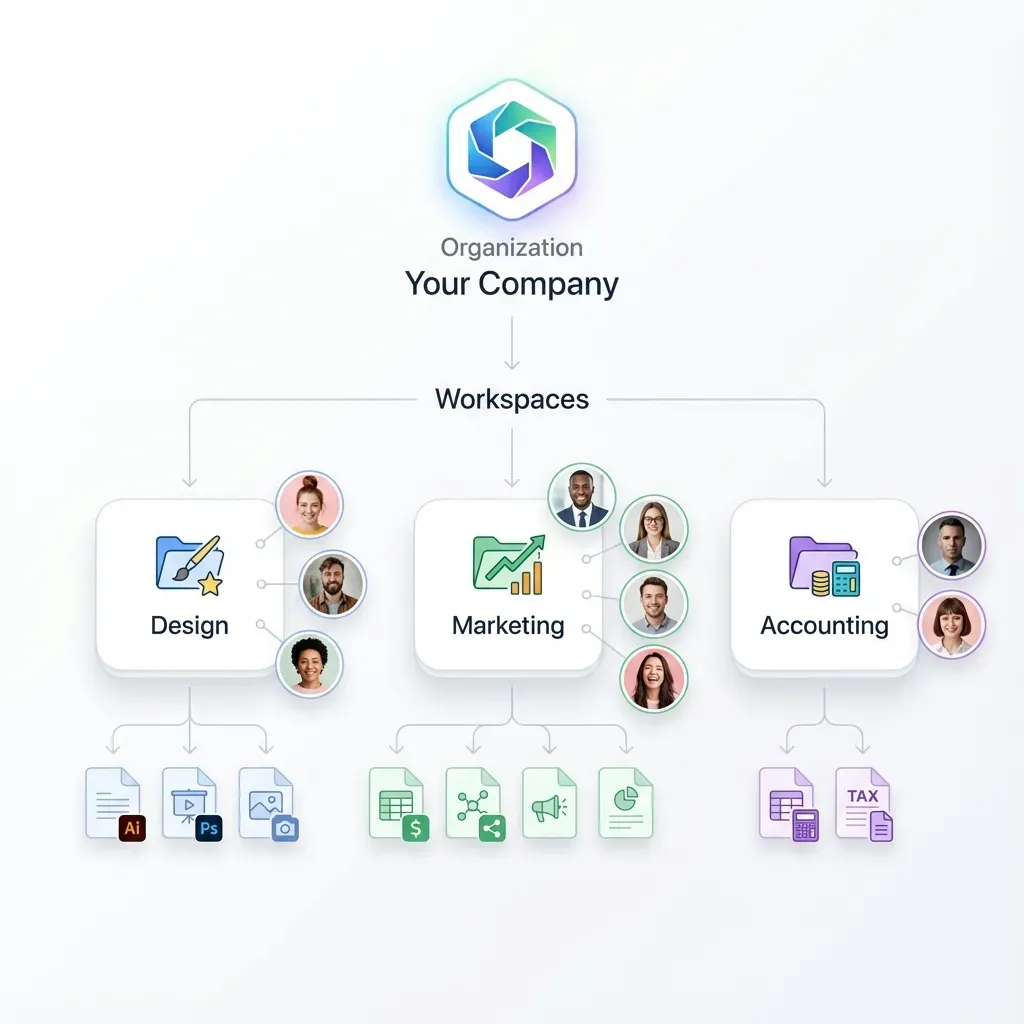

Organize Your Private Credit Diligence in One Workspace

Fastio gives lending teams a secure workspace with granular permissions, audit trails, and AI-powered document search. Start with generous storage, no credit card required. Built for data room private credit workflows.

Folder Structure for Multi-Tranche Credit Facilities

A private credit data room needs a folder structure that reflects how lenders actually review documents. Credit committees work through categories, not chronological uploads. The folder structure should mirror the document checklist above, with some additions for deal-specific materials.

Recommended Top-Level Structure

- Transaction Overview contains the executive summary, term sheet, sources and uses, and deal timeline

- Credit Documentation holds the credit agreement, security documents, intercreditor agreements, and guarantees

- Financial Information includes audited statements, management accounts, projections, and the financial model

- Collateral Package contains the loan tape, borrowing base certificates, appraisals, and UCC filings

- Covenant Compliance holds historical compliance certificates and ratio calculations

- Legal and Corporate includes organizational documents, material contracts, litigation, and regulatory filings

- Existing Debt contains current debt agreements, amendments, and payoff documentation

- Ongoing Reporting is where you place monthly or quarterly updates after the initial diligence phase

Handling Multi-Tranche Structures

Many private credit deals involve multiple tranches with different priority positions. A first-lien term loan, a second-lien facility, and a mezzanine tranche each have different lender groups with different information rights. Your folder structure should account for this.

Create a shared top level for documents that all tranche holders can see (borrower financials, corporate documents, collateral information). Then create tranche-specific folders for documents that are restricted to specific lender groups: pricing terms, intercreditor agreements showing relative priority, and tranche-specific compliance materials. This approach avoids duplicating the entire room for each tranche while keeping sensitive terms appropriately restricted.

For ongoing monitoring after closing, add a reporting folder with subfolders organized by reporting period. Lenders expect quarterly compliance certificates, updated borrowing base calculations, and financial statements delivered on a set schedule. The data room becomes the central repository for all post-closing reporting rather than a tool used only during the transaction.

Permission Models for Lender Groups

Private credit transactions involve multiple parties with different information needs. The borrower, lead arranger, participating lenders, legal counsel, and credit rating agencies each need access to different document sets. Your data room permissions need to reflect those boundaries.

Typical Permission Tiers

Borrower team gets full upload and edit access to all folders. They're responsible for populating the room and responding to lender requests. Keep the borrower team small to maintain document control.

Lead arranger or agent bank gets view access to everything and the ability to invite participating lenders. In a syndicated facility, the lead arranger coordinates diligence and needs visibility into what participants are reviewing.

Participating lenders get view access to shared diligence materials but may be restricted from tranche-specific pricing or terms for tranches they're not participating in. Each lender's credit committee has its own review process and timeline.

Legal counsel typically gets broad view access but should be limited to their client's materials. Borrower counsel and lender counsel should not be able to see each other's internal working documents if those are stored in the room.

Third-party advisors like appraisers, environmental consultants, or accountants get narrow access limited to the documents they need to produce their deliverables.

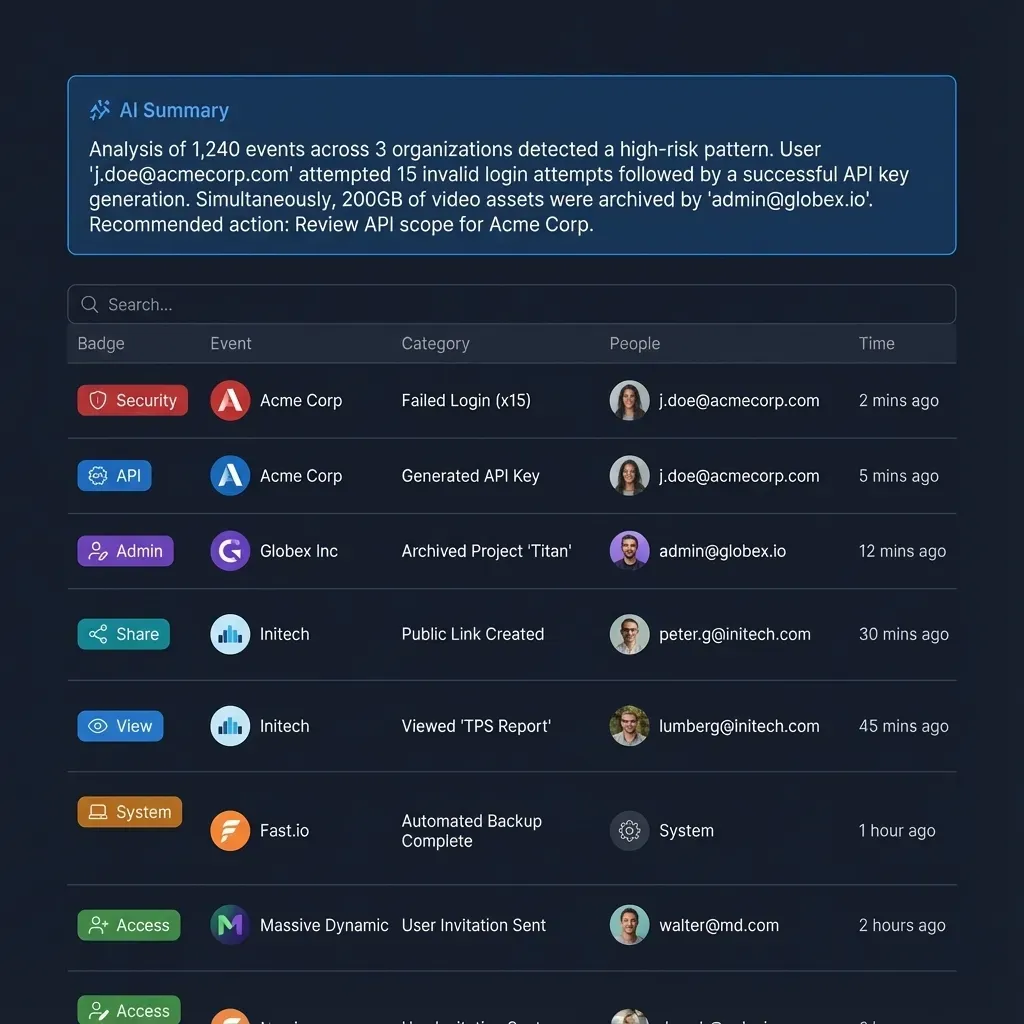

Fastio handles these tiers through granular workspace permissions at the organization, workspace, folder, and file level. You can set different access levels for each group without creating separate rooms, which avoids the version control problems that come from maintaining parallel copies of the same documents. Audit trails track every file view and download, so the borrower can see which lenders are actively reviewing and which haven't started.

For time-limited access, Fastio supports auto-expiring access links. This is useful for participants in a syndication who drop out of the deal. You can revoke their access immediately rather than waiting for someone to remember to do it manually.

How Loan Tapes and Borrowing Base Certificates Work in Data Rooms

Two documents distinguish private credit data rooms from every other type: the loan tape and the borrowing base certificate. If you're setting up a data room for the first time, understanding how lenders use these documents helps you structure the room correctly.

Loan Tapes

A loan tape is a detailed spreadsheet listing every loan or receivable in a portfolio. For a direct lender originating loans, the tape includes borrower names, loan amounts, interest rates, maturity dates, collateral descriptions, payment history, and delinquency status. For asset-backed facilities, the loan tape is the primary collateral document because it defines exactly what secures the lender's investment.

Lenders use loan tapes to run their own credit analysis. They'll sort by geography, industry, loan size, and delinquency status to identify concentration risks. They'll cross-reference payment histories against the borrower's reported cash flows. A clean, well-formatted loan tape accelerates this analysis. A messy one with inconsistent field definitions or missing data triggers follow-up questions that delay the process by weeks.

In the data room, loan tapes should sit in the Collateral Package folder with clear version labels. Lenders expect updated tapes at regular intervals during diligence and after closing as part of ongoing reporting. Use file versioning to maintain a clear history of each update rather than overwriting prior versions.

Borrowing Base Certificates

A borrowing base certificate calculates how much the borrower can draw under a revolving credit facility. It applies eligibility criteria and advance rates to the collateral pool, resulting in a maximum available draw amount. The borrowing base is typically recalculated monthly or quarterly and submitted to the agent bank.

Preparing the first borrowing base certificate in the lender's required format has a steep learning curve, especially when the collateral pool includes hundreds of individual assets. Each asset needs to be categorized, tested against eligibility criteria, and assigned the correct advance rate. Getting this right at closing prevents draws from being delayed or disputed.

Store borrowing base certificates alongside the loan tape in the Collateral Package folder. Historical certificates show the trend in collateral coverage over time, which lenders use to assess the stability of the borrowing base. If the borrowing base has been declining, lenders will want to understand why before committing to the facility.

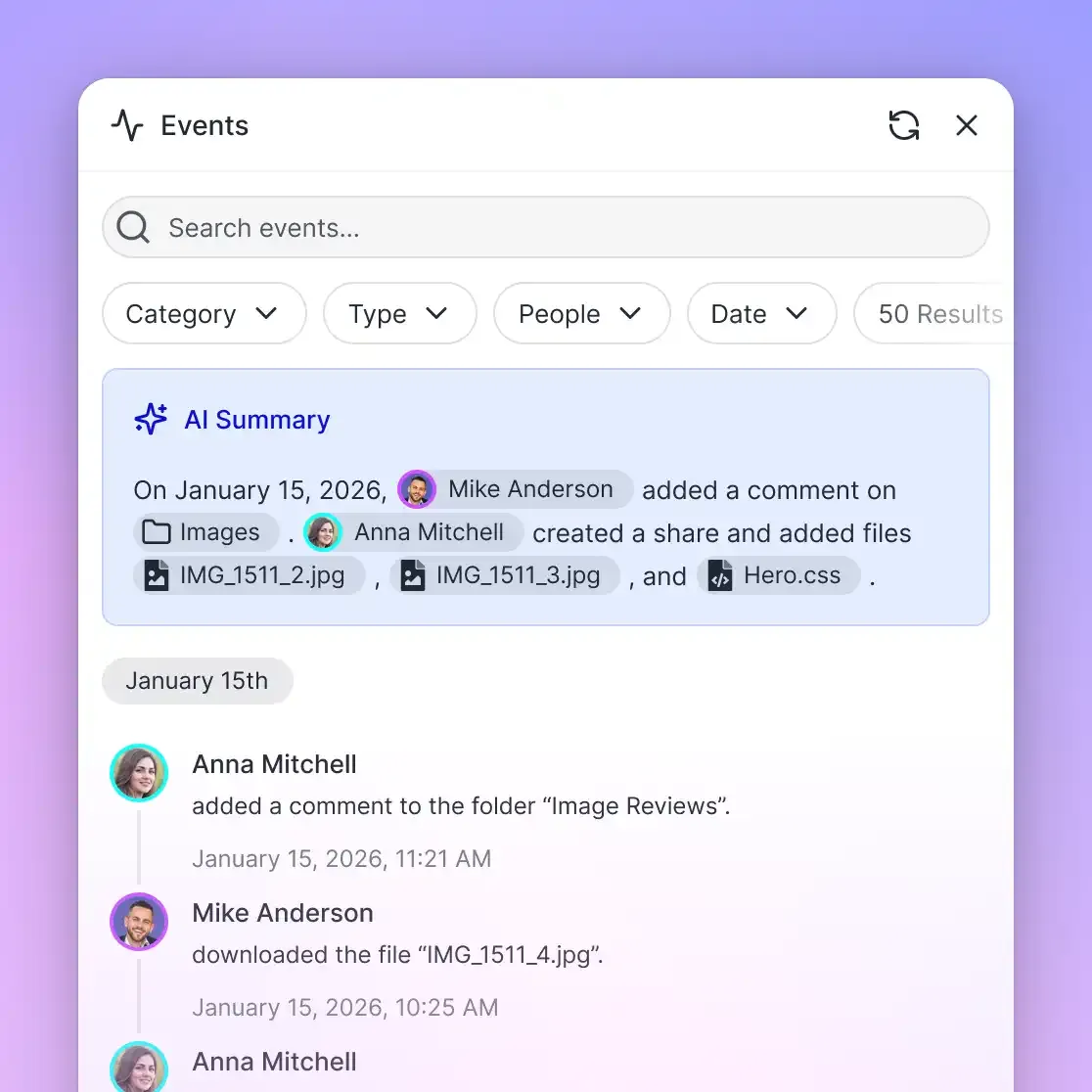

Fastio's workspace intelligence can index these documents once uploaded, making them searchable across the entire room. Instead of manually scanning through monthly certificates to find when the borrowing base first dipped below a threshold, you can ask questions about the documents directly. This is useful during the diligence phase when lenders are reviewing months of historical compliance data.

Tracking Lender Engagement and Managing the Diligence Timeline

Private credit diligence moves on a defined timeline. The borrower needs to know which lenders are actively reviewing, which are falling behind, and which have stopped engaging entirely. Data room analytics make this visible.

What to Track

Document access patterns show which folders and files each lender has viewed. A lender spending time in the financial model and collateral folders is doing real work. A lender who opened the executive summary once and hasn't returned may be losing interest or waiting for internal approval to proceed.

Download activity indicates which documents lenders are taking to their credit committees. When multiple lenders download the same set of files within a short window, it usually means credit committee meetings are being scheduled. That's a signal to the borrower that commitment letters may be coming soon.

Q&A volume by lender tracks which institutions are asking the most questions. Active questioning correlates with serious interest, not skepticism. A lender asking detailed questions about covenant calculations is further along in their review than one asking basic questions about the business.

Managing the Timeline

Most private credit transactions have a target closing date driven by the borrower's financing needs. The data room analytics help borrowers manage toward that date. If a key lender hasn't accessed the room two weeks before the planned closing, the borrower's team knows to follow up rather than assume everything is on track.

For syndicated deals, the lead arranger uses access data to manage the book-building process. They can identify which institutions are likely to commit based on engagement depth and which ones need additional outreach or management meetings.

Fastio's portal analytics track viewer engagement at the document level. You can see which files were viewed, when, and by whom. Combined with workspace activity summaries, this gives borrowers and arrangers a clear picture of diligence progress without requiring manual status calls with every participant.

After closing, the data room transitions from a diligence tool to an ongoing reporting repository. The same permission structure continues to work: lenders access quarterly reports, updated compliance certificates, and amended documents through the same workspace they used during diligence. This continuity eliminates the need to set up a new sharing mechanism for post-closing obligations.

Frequently Asked Questions

What documents do private credit lenders need?

Private credit lenders typically require audited financial statements (three years), a financial model with stress scenarios, a loan tape detailing the collateral pool, borrowing base certificates, the draft credit agreement, intercreditor agreements, security documents, covenant compliance history, corporate organizational documents, and a schedule of existing indebtedness. The exact requirements vary by deal type. Direct lending transactions may require fewer documents than broadly syndicated facilities, which add information memorandums and bank meeting presentations.

How do you set up a data room for direct lending?

Start by organizing documents into categories that match how credit committees review them. Create top-level folders for transaction overview, credit documentation, financial information, collateral package, covenant compliance, legal and corporate documents, and existing debt. Upload the core documents before granting lender access. Set granular permissions so each lender group sees only what they're entitled to. Add an ongoing reporting folder for post-closing deliverables. Use a platform with audit trails so you can track which lenders are actively reviewing.

What is the best data room for private credit funds?

The best data room for private credit depends on your deal volume and complexity. For teams running multiple transactions, look for granular folder-level permissions, audit trails, file versioning, and the ability to handle large document sets without per-page pricing. Fastio offers workspace-level permissions, built-in AI search across documents, and auto-expiring access links, all on a free tier with 50 GB storage. Other providers like Intralinks and Datasite are established in the debt capital markets but charge per-page or per-user fees that scale quickly with large document sets.

How is a private credit data room different from a private equity data room?

Private equity data rooms emphasize narrative materials like pitch decks, growth metrics, and market analysis. Private credit data rooms emphasize verifiability through loan tapes, borrowing base certificates, covenant compliance records, and detailed collateral documentation. The permission structure also differs. PE data rooms typically manage buy-side and sell-side access. Private credit data rooms need to handle multiple lender tiers, tranche-specific restrictions, and ongoing post-closing reporting access.

What is a loan tape and why does it matter for data room diligence?

A loan tape is a spreadsheet listing every loan or receivable in a collateral portfolio, including borrower details, loan amounts, rates, maturities, payment history, and delinquency status. Lenders use it to run independent credit analysis, identify concentration risks, and verify the borrower's reported financial performance. In asset-backed facilities, the loan tape is the primary collateral document. Keeping it clean, consistently formatted, and regularly updated in the data room prevents delays caused by lender follow-up questions.

How long should a private credit data room stay active?

Unlike equity transaction data rooms that close after a deal completes, private credit data rooms often stay active for the life of the credit facility. Lenders expect ongoing access to quarterly compliance certificates, updated borrowing base calculations, financial statements, and any covenant amendment documentation. Plan for the data room to transition from a diligence tool to a reporting repository after closing. This avoids setting up a separate sharing mechanism for post-closing obligations.

Related Resources

Organize Your Private Credit Diligence in One Workspace

Fastio gives lending teams a secure workspace with granular permissions, audit trails, and AI-powered document search. Start with generous storage, no credit card required. Built for data room private credit workflows.